Previously, if people wanted to pass wealth to their children (often prompted by the prospect of ultimately paying inheritance tax if they did not), they would use trusts because then they could keep the assets under their control. More than a decade ago, the government made that option no longer viable for most UK-based individuals by:

- imposing a charge of 20% when assets (over the first £325,000) are put into a trust; and

- making trusts subject to the highest income tax and capital gains tax rates.

For families with assets eligible for relief from inheritance tax – a trading business, a farm or 'risky' investments such as AIM and EIS shares – trusts are still useful, but not so for those holding traditional investments or cash.

If, for whatever reason, a trust or a simple outright gift to children is inappropriate, what are the alternatives? Some years ago, much was made of so-called 'family limited partnerships' and while they remain the right vehicle for some, they are appropriate only for those with at least £10 million to spare because of the financial regulations to which they are subject. Enter the family investment company.(1)

What is a family investment company?

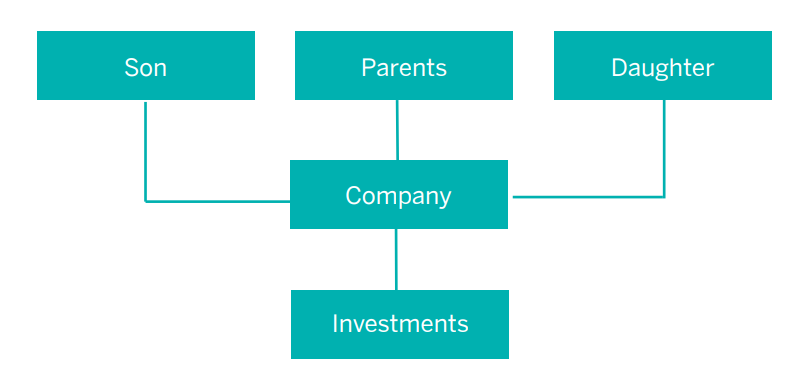

A very simple example of a family investment company is as follows.

The parents create the company and fund it with cash. They are the directors and the holders of all of the voting shares, and their children are given a non-voting share each. That means that if one of the children needs money, the parents can declare a dividend in their favour.

The parents are in complete control of the company, but they have reduced their taxable estates because their shares carry no economic rights, only voting rights. There is a further degree of protection because, while the children hold shares outright, the articles can from the outset prohibit the transfer of shares to anyone who is not a descendant of the parents.

In due course – for instance, when the children are in secure relationships and sufficiently responsible – the parents can bring them onto the board and give them voting shares.

The parents have, therefore, reduced their taxable estates by shifting value to the children, but without handing over control.

In addition, family investment companies are increasingly attractive thanks to their favourable tax status:

- Funding the company carries no tax charge.

- When the company buys stocks, it pays 0.5% stamp duty exactly as individuals do.

- Currently, the company will pay only 19% on any profit that it makes on the sale of underlying investments. Come 2023, that rate will be preserved for companies with profits below £50,000, while larger companies may pay up to 25%.

- When determining the company's taxable profit, the investment manager's fees are deductible.

- Dividends declared on almost any kind of underlying equity are tax free in the company's hands.

- If the company itself declares a dividend, the tax rate depends on the income of the recipient. In the example above, if the daughter is at university and therefore has no income, dividends of up to £14,500 can be paid to her tax free (ie, her dividend allowance of £2,000 plus her personal allowance of £12,500). The next £37,500 will attract only 7.5% tax.

All of the above makes family investment companies appealing. However, there are some limitations:

- If the family are higher rate taxpayers and receive regular dividends from the company, they will be making little use of the benign tax environment that the company offers: to the extent that income from the underlying investments flows immediately through to the family, it will be taxed exactly as if the investments were held directly.

- Although the company is not a one-way street, it can be expensive to undo. If the family wanted to get the assets back into their own hands, they would need to redeem their shares or wind up the company. Doing so would give rise to capital gains tax on the amount by which the shares had increased in value.

The above example is a simple one, suitable for the family in question. No two families are the same, and for another a more complicated entity might be suitable.

Endnotes

(1) Although this article is written from a UK perspective, family investment companies can be just as useful for international clients; a trust is not always the right vehicle and not every family feels comfortable involving a professional trust company.